JemStep provides online advisory services geared to help individuals achieve retirement goals. Founded in 2008, the main idea behind JemStep is to connect to your various investment accounts, look at your current holdings, and recommend specific buy/sell actions to optimize your portfolio. JemStep will provide an asset allocation based on your profile, and for a fixed monthly fee give specific buy/sell recommendations in your portfolio (Unless the portfolio is under 25K for which the recommendations are free.)

Overall, I felt JemStep provided a level of depth in their analysis and recommendations not available from their competitors. At this time, they provide only recommendations and do not execute trades on behalf of online clients. The recommendations are usually simple rebalancing actions once a quarter.

JemStep claims to track more than 2 billion dollars in assets for private clients. I’m usually a little skeptical of these kind of claims. Since they don’t actually manage the money, you could theoretically say you have a portfolio of any size or get advice on a portfolio but not execute the trades. However, this isn’t really relevant for the evaluation of their services which I consider quite good.

Step by step details are provided below about how JemStep works:

Provide Profile and Goals

The first step is to enter some simple profile information most importantly age, target retirement age, salary and yearly retirement savings.

Figure: Provide basic profile information

Figure: Provide basic profile information

Another important component is to enter your self-assessed risk profile. This is the most critical factor JemStep uses in determining your recommendations. All online investment advisory services include risk profiles with around 5 classifications ranging from conservative to aggressive. To help select your profile, each classification is shown with best and worst case scenarios of portfolio performance based on historical patterns. This is a fairly general way to derive a portfolio and obviously doesn’t result in particularly personalized advice but nonetheless even with live advisors, this is the common model as it’s the easiest and cheapest to implement.

Figure: Specify your risk profile and also Mutual Fund and ETF investment type preference

Figure: Specify your risk profile and also Mutual Fund and ETF investment type preference

You are given the option to use ETFs or Mutual Funds. Jemstep’s preference is to select from both Mutual Funds and ETFs to pick the best funds. JemStep takes into account fees in making recommendations.

You can also can specify to use actively managed funds but the recommendation is for passive funds.

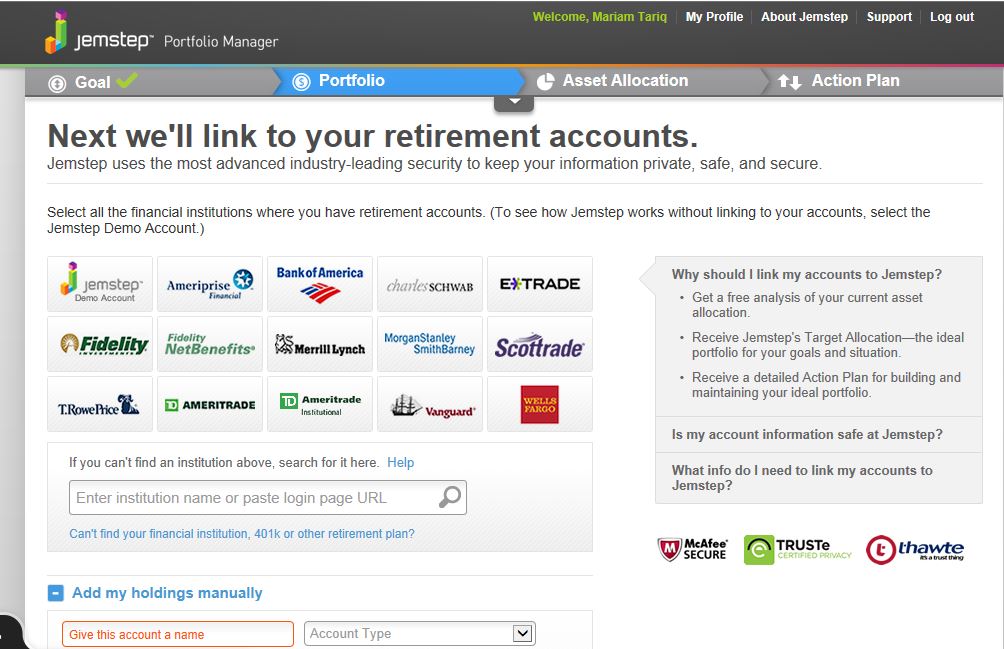

Connect to Existing Accounts

The next step is to allow JemStep to connect to your investment accounts by providing your user/login credentials. As with other services, the credentials are not stored and the process is secure (this is the claim). Especially, in light of recent online and in-store security breaches, one can never be 100% sure of security. I personally have not overcome my concerns. Therefore an option is provided to enter this information manually. Since JemStep will mostly likely recommend you change most of your existing portfolio, the manual option while tedious is sufficient to move ahead in the process.

Figure: Either provide credentials to your investment accounts, or enter your portfolio data in manually

Figure: Either provide credentials to your investment accounts, or enter your portfolio data in manually

JemStep will analyze your current holdings across different accounts to make recommendations.

Determine Asset Allocations

JemStep then runs your input data through its engines to determine the most appropriate asset allocation model for you. I surmise that they likely have a fixed number of models and match each client to the best one. The asset allocation determines the broad categories where you will invest (such as US stocks, international, commodities etc.) and the percentage of your portfolio to invest in each.

Figure: JemStep shows all the steps it goes through in coming up with the asset allocation

Then JemStep shows the asset allocation recommendation compared to your current portfolio.

Figure: Asset allocation showing the difference between your current and recommended target allocations

Figure: Asset allocation showing the difference between your current and recommended target allocations

Recommendations

JemStep then determines what funds to sell completely or in part from your existing portfolio and what to buy instead.

While the asset classes are similar to that of other advisory services, the key part – the actual ETFs and Mutual Fund portfolio components- vary greatly between services. I found that JemStep provides fairly detailed information about their recommendations. For example, JemStep actually looked closely at my current holdings. Instead of taking the simplest approach of selling off all my holdings to purchase their recommendations (like FutureAdvisor), they allowed me to keep some of holdings of a fund but balanced it out with their suggestions.

Figure: JemStep shows you the steps it undertakes to determine the specific recommended holdings including buy/sell actions for your portfolio

Figure: JemStep shows you the steps it undertakes to determine the specific recommended holdings including buy/sell actions for your portfolio

JemStep has its own ranking system for funds. I’m sure this is algorithmic based on their own criteria looking at fund performance and other published factors. It simply wouldn’t scale for them to analyze every fund. The analysis provided seemed decent. They provide good detail about their recommendations, choosing funds that they rank at the top of their list (as opposed to using an third party like Morningstar). The information was fairly detailed about rationale.

I tried MarketRiders portfolio as my existing portfolio to which they suggested improvements – slight ones over MR portfolio US stocks.

Figure: Action Plan shows specific buy/sell actions with explanations.

Figure: Action Plan shows specific buy/sell actions with explanations.

For comparison, I went back to the first screen to change my criteria to use ETF and Mutual Funds (as opposed to only ETFs). The results were slightly different. You might want to choose this option if holding the account in a tax-deferred or tax-exempt account.

Figure: Mutual Fund and ETF Recommendations

Figure: Mutual Fund and ETF Recommendations

It’s clear that the guidance provided is computerized and not personalized at a 1-to-1 level. For example, I had one allocation in my current portfolio that was 1% off the target (as shown in the above asset allocation screenshot, my US stocks allocation was 52% vs 51%). The rationale provided was obviously canned – “Based on your financial situation, JemStep’s analysis of your current portfolio shows that it’s weighted too heavily in U.S. equities.”

Despite this, I still found a lot of the information helpful. There is a lot of data and algorithms to back their suggestions. They also provide useful charts such as simulating the average and worst case scenarios of portfolio performance. This kind of data is nothing to act on but it’s still good to have perspective on the content of your portfolio and for your own education to understand the rationale behind it.

Pricing

JemStep has tiered pricing based on the size of your portfolio. If the portfolio is under 25K, the service is free and you can get the specific buy/sell recommendations. The next tier is 17.99 a month for a 100K portfolio. There is a promotion for first 3 months for 17.99. Then 17.99 a month thereafter. This amounts in $215 a year which I think is reasonable.

For all size portfolios, you can get a free evaluation of your current portfolio that will tell general things like where you are over or underexposed or not covered, but it doesn’t show any recommendations unless you pay. The asset allocation suggestions are not actually very useful. You need the specific funds. They follow very standard asset allocation models which can be found with free tools from most brokerages.

Positives

JemStep’s interface is well designed and easy to follow. Their recommendations are more detailed than other services out there. For example, they take into consideration different factors like taxable and non-taxable account.

While they don’t offer trade execution, the trading actions require rebalancing only once a quarter. Furthermore, JemStep will tell you exactly what actions to take and when.

I also like that they are cautious to check if how long you’ve held a position before selling it to ensure you don’t incur penalties.

Negatives

The main negative is that unlike other services like MarketRiders, they do not provide recommendations specific to brokerages. Therefore, you are likely to incur more trading fees if your brokerage charges for certain funds. For example, JemStep provides many Vanguard recommendations. It’s free to buy Vanguard funds in a Vanguard account but not Fidelity. But on the flip side, buy and sell actions occur only 4 times a year.

The fact that they don’t execute trades could be a negative for some. However I will gladly forgo that option in lieu of lower cost. Following asset allocation models to does not require frequent trading.

Some additional insights would be appreciated in terms of what to expect in the future would have been nice. For example, do they adjust the holdings as market conditions change or stick to the same holdings

They do say they will make adjustments in allocation and risk based on your age. This I would expect. But it’s not clear if they would make more significant changes in portfolio based on market drivers. I suspect like the other tools, that they follow a simple asset allocation model based on Modern Portfolio Theory.

Bottom Line

I like JemStep. It’s the most comprehensive of its direct competitors. It’s reasonably priced. Information is detailed but what I like is that the management process is still easy. The details aren’t essential to self-management. If you want the details behind their rationale, it’s available.